In today's world, where identity theft and credit fraud are all too common, it's essential to take steps to protect yourself. Two commonly used methods are credit freeze and credit lock, but there is also a credit fraud alert. These three are often used interchangeably, but there are significant differences between them.

What is a Credit Fraud Alert?

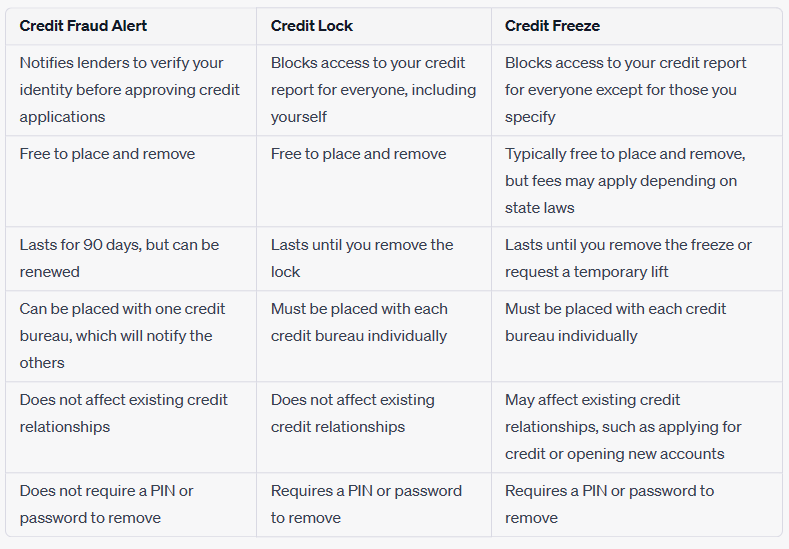

A fraud alert is a notice placed on your credit file, warning lenders and creditors to take extra steps to verify your identity before extending credit in your name. The alert informs them that you may be a victim of identity theft, and they should take steps to verify your identity before issuing credit. This process is free and can be requested from any of the three major credit bureaus – Experian, TransUnion, and Equifax.

There are three types of fraud alerts:

1. Initial Fraud Alert

An initial fraud alert remains on your credit report for one year and notifies creditors to verify your identity before issuing credit in your name.

2. Extended Fraud Alert

An extended fraud alert remains on your credit report for seven years and requires creditors to take additional steps to verify your identity before issuing credit in your name.

3. Active Duty Military Alert

This alert is for active-duty military personnel who are deployed away from home. This alert remains on your credit report for one year and notifies creditors that you may be a victim of fraud, and they should take additional steps to verify your identity before issuing credit in your name.

The advantage of a fraud alert is that it doesn't restrict access to your credit file. You can still open new accounts or apply for credit without removing the alert. However, you'll need to provide additional information to verify your identity when you do so.

What is a Credit Freeze?

A credit freeze, also known as a security freeze, is another method of protecting your credit. A credit freeze restricts access to your credit file, making it challenging for identity thieves to open new accounts in your name. Once you've placed a credit freeze, lenders and creditors won't be able to pull your credit report or issue credit without your permission.

To place a credit freeze, you need to contact each of the three credit bureaus – Experian, TransUnion, and Equifax – individually. You'll need to provide personal information, such as your name, address, Social Security number, and date of birth. There is a small fee to place a credit freeze, and you'll need to pay the same amount to lift the freeze temporarily or permanently.

A credit freeze remains in effect until you lift it, but it doesn't expire automatically like a fraud alert. You can lift the freeze temporarily if you're applying for credit and want to give lenders access to your credit report. However, you'll need to lift the freeze for a specific period and reinstate it afterward.

What is a Credit Lock?

A credit lock is a security feature offered by credit bureaus that allows you to restrict access to your credit reports. Unlike a credit freeze, a credit lock can be quickly turned on or off, making it easier to access your credit report when you need it.

A credit lock provides a higher level of convenience compared to a credit freeze. You can easily lock or unlock your credit report online or via a mobile app. You may also set up a credit lock through a credit monitoring service.

A credit lock works by blocking access to your credit report. This means that if a lender or creditor tries to access your credit report, they won’t be able to see it. However, unlike a credit freeze, a credit lock only applies to the credit bureau that you have locked. Therefore, you’ll need to lock your credit report at each of the three credit bureaus for comprehensive protection.

One significant advantage of a credit lock is that it allows you to lock and unlock your credit report instantly, giving you greater flexibility when it comes to applying for credit. This makes it an excellent option for people who are actively applying for credit, such as a new credit card, auto loan, or mortgage.

However, like credit freezes, credit locks are not entirely foolproof. Although they can help prevent fraud, they may not stop all attempts to steal your identity or misuse your credit. Therefore, it’s still essential to monitor your credit reports regularly and keep an eye out for suspicious activity.

Which One Should You Choose?

Remember, the option you choose will depend on your individual needs and circumstances. Consider your level of risk for identity theft, your credit activity, and your comfort level with limiting access to your credit report.

Can You Have Any of them At the Same Time?

You can have both a credit freeze and a fraud alert on your credit report at the same time.

A fraud alert notifies creditors to take extra precautions when verifying your identity and credit, while a credit freeze restricts access to your credit report altogether. By having both in place, you can add an extra layer of protection against identity theft and credit fraud.

You cannot have a credit lock and a credit freeze at the same time with the same credit bureau. This is because a credit lock and a credit freeze are essentially the same thing – they both restrict access to your credit report to prevent identity theft and fraud. However, some credit monitoring services may offer both options as part of their package. It's important to note that having both a credit lock and a credit freeze at the same time with different credit bureaus can provide an extra layer of protection.

Final Thoughts

Overall, credit freezes, credit locks, and credit fraud alerts are useful tools that can help protect you from identity theft and credit fraud. Each one has its advantages and disadvantages, so it’s essential to consider which option is best suited for your situation.

If you’re concerned about identity theft and want the most comprehensive protection, a credit freeze may be the best option for you. It provides the most protection since it restricts access to your credit report entirely. However, keep in mind that you'll need to lift the freeze whenever you want to apply for credit or loans.

If you're looking for a more convenient option that still provides some level of protection, a credit lock might be a better choice. It’s easier to use and can be unlocked in real-time, making it an ideal option if you're actively applying for credit. However, keep in mind that it may not provide as much protection as a credit freeze, as it’s not regulated by law.

If you're not sure which option to choose or are looking for a temporary solution, a credit fraud alert might be the best choice for you. It’s free and easy to set up, and it notifies you whenever someone tries to access your credit report. However, it does not prevent someone from accessing your credit report entirely.

Ultimately, the choice between credit freezes, credit locks, and credit fraud alerts will depend on your specific situation and needs. We hope this guide has helped you understand the differences between each option and make an informed decision about which one to choose.

Remember, protecting your credit is essential, so take the necessary steps to ensure your financial security.